Lihat juga

11.06.2026 12:56 PM

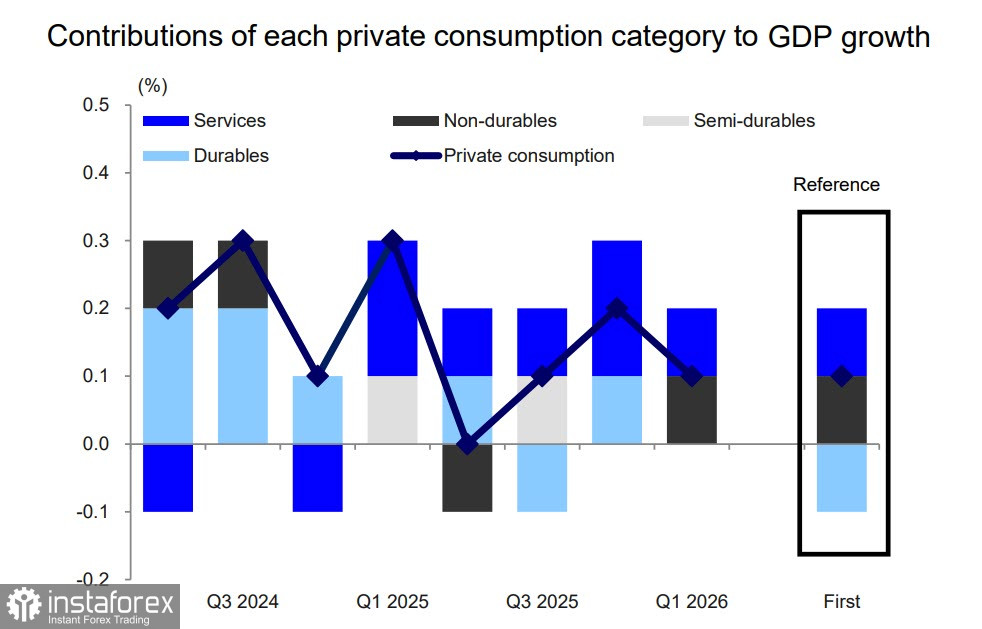

11.06.2026 12:56 PMReal GDP growth in Q1 was slightly revised downward to +0.5% q/q and +1.8% y/y, compared with the initial estimate of +0.5% and +2.1%. The first quarter only partially reflected the onset of the US–Israel–Iran war, but at this stage there appears to be no direct threat of a sharp slowdown due to disruptions in energy supply chains. The second quarter is likely to be affected more significantly by this factor, but current estimates remain relatively optimistic, as geopolitical tensions are expected to ease and oil prices are projected to gradually decline.

Support for a rate hike is already gaining momentum among members of the Monetary Policy Board, and it now appears likely that the executive branch will also support an increase. Regarding the position of the Takaichi administration, which is likely the main obstacle to a final decision on a rate hike, Jiji Press reported that US Treasury Secretary Scott Bessent advised Prime Minister Takaichi during a meeting not to block a Bank of Japan rate increase. Therefore, it is reasonable to conclude that it is now more likely that the administration will accept—or has already accepted—a rate hike.

Key risks ahead of the meeting include events that could complicate a rate hike decision. These include severe supply chain disruptions caused by further escalation of tensions in the Middle East. However, such a deterioration in conditions appears unlikely in the coming days.

Analysts at Mizuho Bank forecast that the Bank of Japan will raise rates approximately once every six months. The policy rate is expected to reach 1.25% by December 2026 and 1.50% by June 2027 (terminal rate). In parallel with rate hikes, the Bank of Japan is also likely to slow the pace of quantitative tightening.

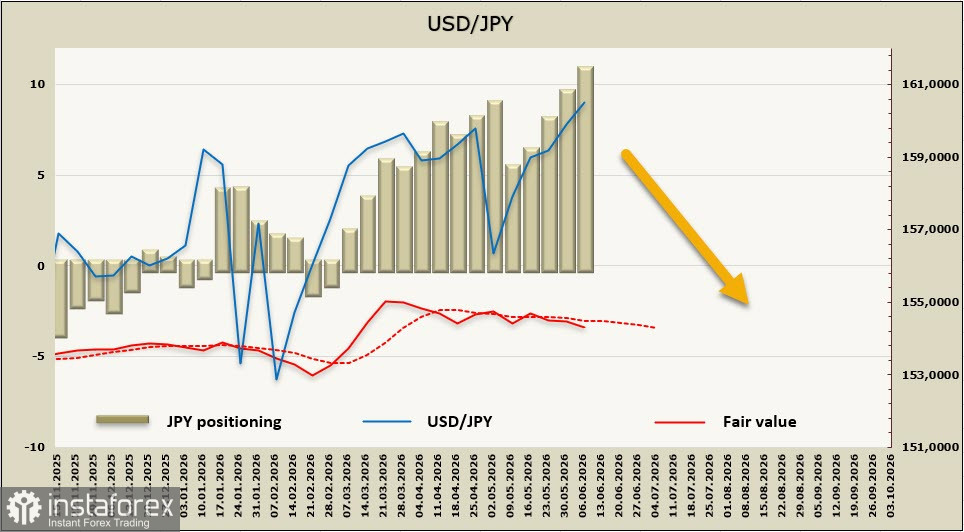

The net short position in the yen increased by 1.13 billion over the reporting week, reaching -10.13 billion. Short positions have exceeded the previous 2007 peak and reached a new record high. The fair value estimate is attempting to move below the long-term average.

USD/JPY has moved close to the April 30 high, after which a large-scale currency intervention followed. The current situation is similar; however, if the Bank of Japan proceeds with a rate hike, another intervention may not be necessary. Japanese authorities may also be considering a similar scenario and may retain the option of intervening later if the yen does not stabilize. Fundamentally, the yen remains weak, and a move toward 162 is still in play. However, confidence in a rate hike could support bearish USD/JPY positioning and allow the yen to retrace a few figures lower.