यह भी देखें

16.07.2026 07:02 PM

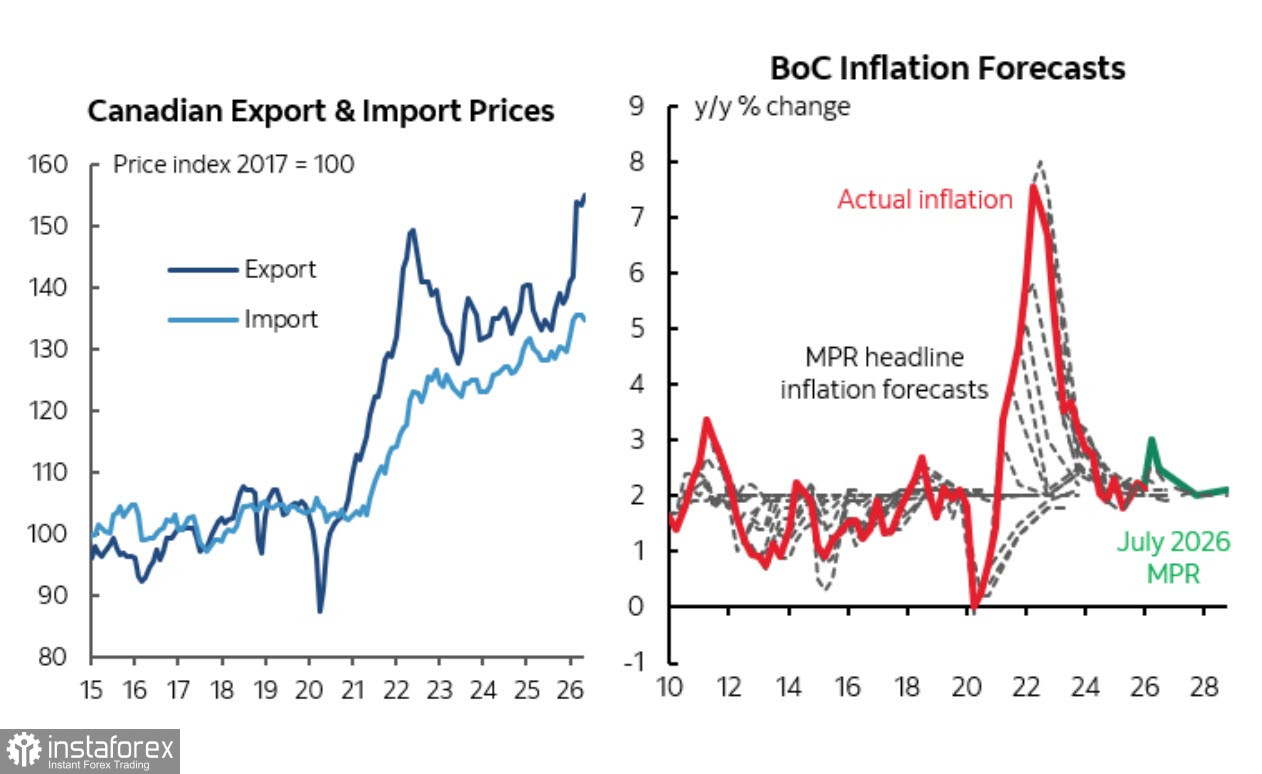

16.07.2026 07:02 PMJune's labor market report from Statistics Canada delivered moderately positive signals. Employment increased by 18,000, surpassing analysts' expectations of 10,000, while the unemployment rate fell to 6.5%, its lowest level since January 2026. This marked the second consecutive monthly decline following the rise in unemployment to 6.9% in April. However, these figures mask an important detail: employment growth occurred against the backdrop of a declining Canadian population, driven by tighter immigration policies. Meanwhile, the manufacturing sector lost 17,000 jobs (-0.9%), bringing the cumulative decline since January 2025 to 61,000 jobs (-3.2%)—a direct consequence of the trade war with the United States.

In its July policy statement, the Bank of Canada noted that "after a year of weakness, Canada's economy is showing signs of improvement." Nevertheless, the outlook remains cautious. The Bank revised its 2026 GDP growth forecast down to 0.7%, from 1.2% projected in April, while expecting stronger growth only in the second half of the year.

At its July 15 meeting, the Bank of Canada kept its benchmark interest rate unchanged at 2.25% for the sixth consecutive meeting, in line with market expectations. However, its policy tone became more dovish. At the previous two meetings, Governor Tiff Macklem had warned that consecutive rate hikes could become necessary if the conflict in the Middle East continued to push energy prices higher. That language was removed from the July 15 statement, along with the warning that interest rate cuts could be considered if the United States imposed severe trade restrictions. Markets now assign roughly a 40% probability to a 20-basis-point rate hike by year-end, which could weigh on the Canadian dollar, as expectations for Federal Reserve policy continue to become increasingly hawkish.

High oil prices have a mixed impact on the Canadian economy. On the one hand, they boost export revenues, increase profits for energy companies, and support government tax receipts. On the other hand, they reduce households' real incomes and weaken consumer spending. Consequently, any escalation of tensions in the Strait of Hormuz remains the key external risk. A prolonged disruption would likely intensify inflationary pressures while further weakening domestic demand. An economic recession in the United States would pose an even greater threat to Canada, given that approximately 75% of Canadian exports are destined for the U.S. market.

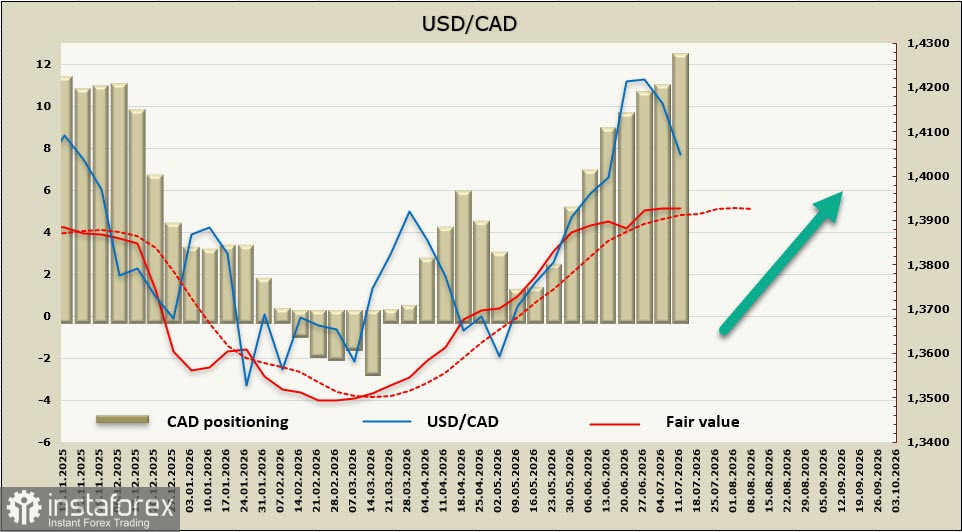

The net speculative short position in the Canadian dollar increased by CAD 1.57 billion during the latest reporting week to CAD -12.19 billion, indicating that speculative positioning remains firmly bearish. At the same time, the estimated fair value remains above its long-term average.

After reaching a 15-month high of 1.4248 at the end of June, USD/CAD entered a corrective phase and is now approaching a test of the lower boundary of its symmetrical triangle near 1.4000. A daily close below this level would open the way toward 1.3970, followed by 1.3850. However, this scenario currently appears less likely and would require further gains in oil prices alongside renewed signs of weakness in the U.S. dollar. Over the longer term, we expect the correction to conclude, with support in the 1.3950–1.3970 level likely to hold before the pair resumes its upward move toward 1.4248.