Vea también

29.04.2026 02:38 PM

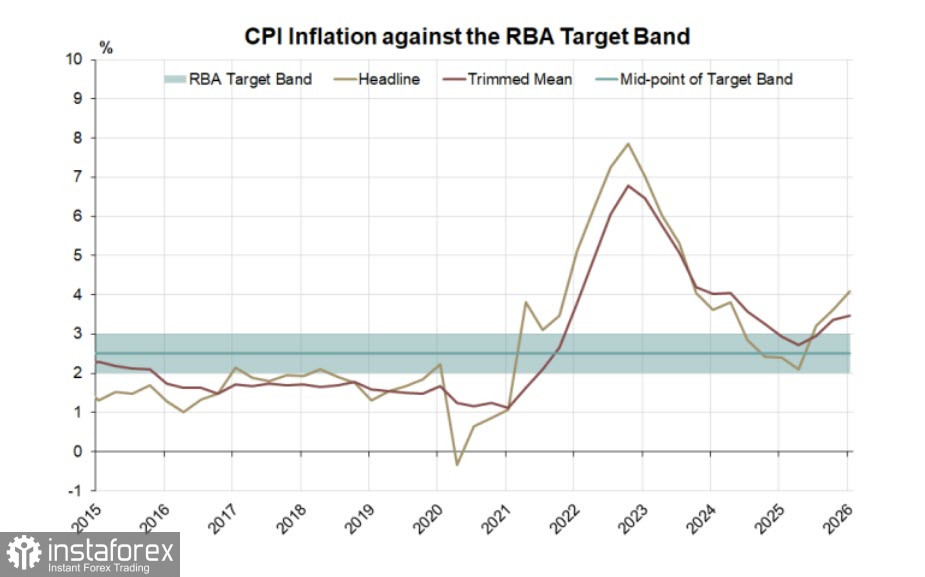

29.04.2026 02:38 PMThe consumer price index in Australia rose by 1.1% in March, pushing the annual CPI rate to 4.6%. This result is slightly below the 4.8% forecast but represents the highest reading in the short history of the monthly inflation series. Quarterly inflation rose to 3.5% and has remained above the target for a second consecutive quarter.

The probability of an RBA rate hike at the upcoming meeting on 5 May has fallen from 80% to 70%, meaning the market still expects a hike, but with less confidence. The inflation report was compiled before fuel excises were cut — one of the government's measures to curb price growth — and, as it turned out, that measure had no impact on diesel, where shortages are intensifying: the average price in March was 2.99 AUD per liter, versus 2.63 AUD in February. At the March meeting the RBA raised the cash rate to 4.1%, and it is clear that inflation will continue to rise, so the RBA will likely have to tighten again. However, the risk that further tightening could trigger a domestic economic crisis, compounding the energy shock with tighter financial conditions, may force the RBA to pause.

The situation remains highly uncertain. In Q4 last year Australia's GDP grew by 2.6% year on year, the fastest pace in two years. Things appeared to be on track, and inflation seemed contained, but the war in the Middle East changed everything. The US and Iran are far from a peace deal; Iran's Supreme Leader Khamenei refused to resume talks, citing US "arrogance," and President Trump, in turn, instructed aides to prepare for an extension of the blockade of the Strait of Hormuz. It appears the strait is being contested by both sides, which reduces the likelihood of a near-term resumption of traffic each day. Most likely, the brief period of rising risk appetite is ending, and the world must prepare for a deeper and more prolonged crisis. This outlook is particularly serious for Australia, given its heavy reliance on external fuel supplies.

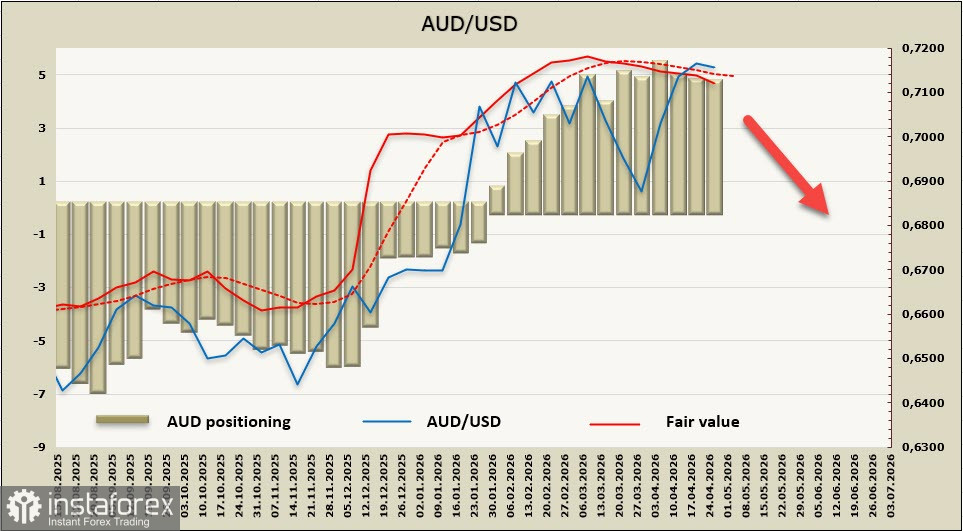

Speculative positioning in AUD was unchanged over the reporting week, with a bullish net exposure of 4.8 billion, but the implied price, pressured by short-term factors, is moving progressively below the long-term average.

A week ago, we assumed AUD/USD would continue to trade in a sideways range, because the likelihood that the RBA would pause at the next meeting was high. Over the past week additional factors have emerged that increase the odds of a southward move. We expect that even the inflation rise will recede into the background in the face of the risk of a sharp economic slowdown and that AUD/USD will turn down toward 0.6915–0.6945.